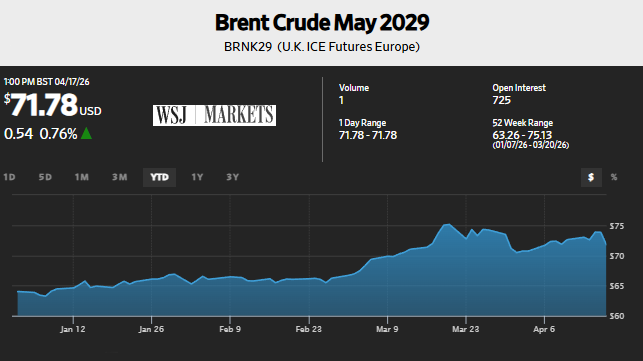

Oil markets have been noisy. Brent has whipsawed on Middle East headlines but for the deepwater market, spot volatility is largely a distraction. The contracts that matter most for the market are being signed against $70 long-dated futures, and the project economics at that level are constructive. This 7G Drillship Market Update covers recent contracting, dayrates, utilization outlook and the US Gulf drillship market.

Futures curves are not a forecast but instead function as a capital allocation signal. If an oil major can earn an IRR above its cost of capital at $71/bbl, it can hedge forward production at that level, sanction the project and create shareholder value with successful execution. At $70 Brent, deepwater delivers and the long-term structural case is improved given countries’ greater need for energy security from recent market disruptions.

One underappreciated impact of the Middle East conflict is SPR rebuilding. Whatever the war’s ultimate resolution, governments that drew down strategic reserves will need to refill them. That demand is a quiet support for the long end of the curve and by extension, for deepwater investment economics.

Deepwater decisions are not made directly on spot price moves. When a rig contract is announced with a term of a year or longer, it’s the visible endpoint of a project cycle that began years earlier with long-lead equipment ordered, infrastructure commitments made and sanction thresholds cleared. Elevated spot prices support oil major cash flows and budgets, but deepwater isn’t a short-cycle business. There’s no version of this market where spot $90 Brent triggers drilling and production within 60 days.

7G Drillship Dayrates: Finding a Floor

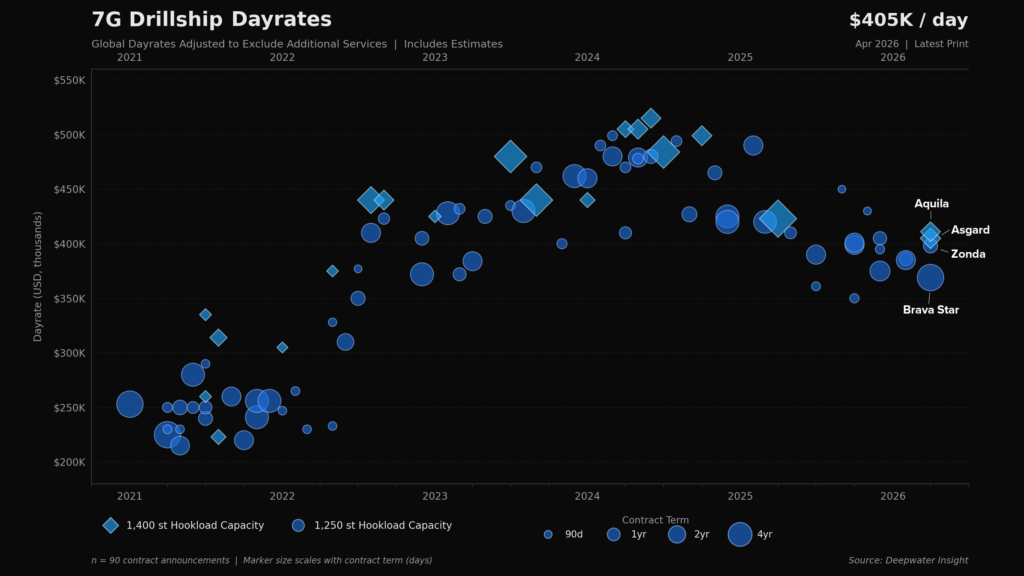

The most telling data points include recent Petrobras awards and Transocean’s Deepwater Asgard. On April 16, 2026, Transocean announced a new contract for Asgard in the East Mediterranean Sea to commence in 4Q26 at a dayrate of $405k. In June 2024, Transocean announced a 365-day contract for Asgard at $515k in the US Gulf, representing the market cycle potentially from peak to trough.

The Petrobras major tenders and Renecon process wrapped up in April. Dayrate expectations heading in were muted — the process launched in summer 2025 against a soft utilization backdrop — but outcomes were better than some feared. The 7G awards averaged above $400k/day for Deepwater Aquila and Atlantic Zonda, while Brava Star came in at $369k (excluding MPD). Adjusting for Constellation’s structural cost advantages as a regional driller, that number is comfortably above $400k on a like-for-like basis.

After peaking in summer 2024, 7G dayrates pulled back. However, the chart above shows support firming. Current utilization in the low 80% range explains the softness, though deepwater’s long-cycle nature provides visibility: projects already awarded, plus likely awards not yet announced, put 7G utilization on a credible path toward ~89% by early 2027. A challenge 7G drillships have is they also compete against high-end 6G drillships also capable of development drilling work in various regions, including Stena Drilling’s fleet of four 6G drillships.

Transocean Plays Defense in the US Gulf

Deepwater Asgard’s new award relocates the rig from the US Gulf to the Eastern Mediterranean — a meaningful market balance move. The company already has Deepwater Conqueror and Deepwater Proteus coming available in the US Gulf in 2H 2026, with Deepwater Atlas adding further availability in early 2027 before its 2-year, $635k/day bp contract begins in June 2028. All three are top-10 ranked drillships, but that’s a meaningful concentration of marketed supply in a single region. Moving Asgard out tightens the US Gulf picture and improves the dayrate environment for the rigs that remain.

Noble’s April 2025 Shell awards provide useful context for the Asgard move. Noble Voyager and Noble Venturer — currently idle and working in West Africa, respectively — are returning to the US Gulf under long-term Shell contracts, effectively replacing Deepwater Proteus (rolling off May 2026) and Deepwater Pontus (October 2027). Shell’s preference for performance-based incentives and options in the new deals were apparently terms Transocean was not willing to match.

The net effect is additional Noble supply entering the US Gulf, which reinforced the logic of repositioning Asgard elsewhere. Transocean managed the move cleanly, limiting downtime and mob/demob costs covered by the undisclosed operator.

The US Gulf: Mature Basin, Frontier Technology

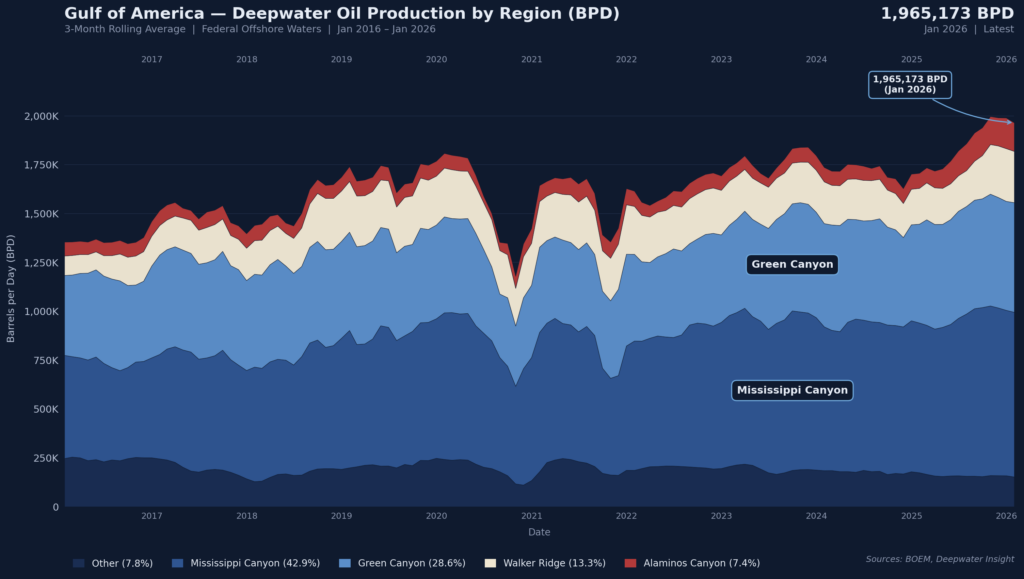

The US Gulf is often characterized as a mature basin, but deepwater production has grown to roughly 2 million bpd as of late 2025, a function of the region’s technological strength rather than resource exhaustion. Transocean’s highest-specification assets, including its 8G drillships capable of 20,000 psi completions, are concentrated here and have been central to that production growth. Chevron’s Anchor and Beacon/Navitas’ Shenandoah are notable examples of technology enabling drilling and completion productivity and well results.

Shell has been one of the US Gulf’s most significant drillship consumers, anchoring Transocean’s fleet with long-term, high-specification contracts that effectively kept the company solvent through the 2015–2021 downturn. Those rigs supported Shell’s success across Perdido, Whale, Appomattox, and ongoing drilling at the mature Mars complex in Mississippi Canyon. Shell sanctioned Sparta in December 2023, a 20k psi project expected to produce first oil in 2028.

As the US Gulf digests its 2024–2025 production additions, a key watch item for 2027 capital budgets is Blackstone’s likely exit from Beacon Offshore. Beacon operates the high-profile Shenandoah 20k project — with Navitas Petroleum holding a 49% non-operating stake — and the asset would draw credible interest from most US Gulf operators. Who ultimately acquires Beacon could have meaningful implications for drilling demand in the region.

Ventura Offshore Update

Following the Petrobras awards, I flagged Ventura Offshore as potentially needing an equity raise after back-of-the-envelope math on their liquidity, material capex needs in 2026 and debt service requirements. The company moved quickly to address the concerns — executing a $75mm tap of its existing notes (bringing the balance to $190mm, a manageable debt load), amending the bond to defer three $10mm quarterly amortization payments to maturity and extending Carolina’s contract to push out its SPS costs. The ~$30mm MPD upgrade on Victoria isn’t due until before contract commencement in early 2027. Taken together, Ventura managed its liquidity well and demonstrated valuable capital markets execution for equity.

Comments (0)

Log in to leave a comment

Sign in