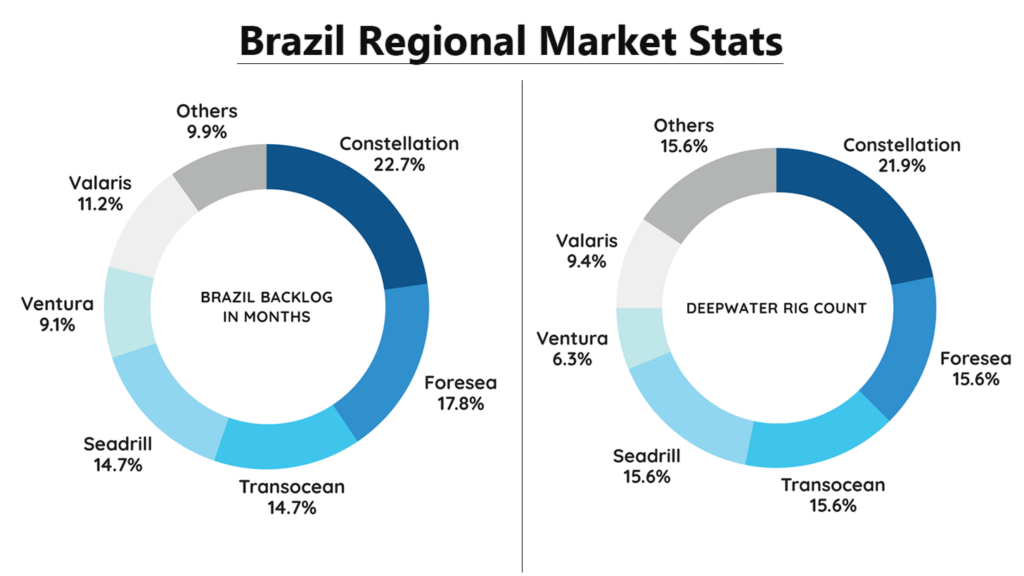

Brazil represents approximately 20% of global deepwater rig demand, and Petrobras has concluded its most significant contracting cycle in years. The Búzios and Mero field tenders, outstanding since mid-2025 and expected to close by year-end, were delayed in part by the concurrent ‘Renecon’ renegotiation process, through which Petrobras sought operational cost efficiencies amid a weaker 2025 oil price environment. The combined result: over $3.6 billion of new deepwater rig commitments, with modest near-term dayrate reductions exchanged for multi-year contract extensions across the fleet.

The recent awards reflect varying rig specifications and cost structures, with Brazilian contractors benefiting from lower domestic operating costs. Adjusting for these regional differences, effective dayrates range from approximately $360k to $430k depending on specifications and contract tenor, with MPD-equipped higher-specification rigs gravitating toward the $400k level. Given that these contracts were negotiated during a softer market, the combination of higher oil prices and accelerating industry consolidation suggests long-cycle deepwater contracting dayrates have room to improve from current levels.

Key big picture takeaways from the results:

- Despite initial concerns over dayrate reductions, the awards are consistent with prior driller commentary that rate concessions would be coupled with meaningful extensions. Sixth-generation drillships and semisubs demonstrated this dynamic, securing long-term extensions in exchange for modest near-term rate reductions. Seventh-generation units, however, accepted shorter extensions of approximately 365 days.

- Petrobras opportunistically leveraged white space on driller schedules, securing favorable terms including dayrate reductions, early termination options after 2.5 to 3 years, and payment deferrals that improve near-term cash flows. The Renecon process also provided operational insights from service providers that should enhance E&P returns. Petrobras further benefits from the presence of regional drillers who prioritize utilization over dayrate maximization, a dynamic that often works in the Brazilian oil major’s favor.

- The Petrobras tender and Renecon process reveal a divergence in international contract driller strategy between rig specs. 6G drillships were extended on long-term contracts at modest dayrates, while 7G units took shorter extensions and some appear to be exiting Brazil for more lucrative international markets. Seadrill appears to be moving the 7G West Carina out of the market, and Noble’s 7G Faye Kozack, whose Petrobras contract ends January 2027, was absent from both the tenders and blend-and-extend agreements as of April 6, 2026. This suggests drillers are more bullish on 7G dayrate prospects outside of Brazil over the longer term.

- Offshore contract drilling is driven by regional market characteristics, and Transocean’s April 2nd announcement of $1 billion in new awards across three rigs illustrates this. 6G NCS-eligible semisub Transocean Barents earned a $450k/day dayrate on a 1,095-day contract with Vår Energi in Norway, well above rates in the Brazil tenders. The divergence reflects Norway’s structurally tighter supply-demand balance, where a smaller pool of NCS-eligible rigs faces competition from fewer drillers, compared to Brazil’s deeper market with regional drillers and a single dominant operator in Petrobras.

7G Drillships: Shorter Extensions, Higher Optionality

Constellation Oil Services’ 7G Brava Star was included in the Búzios tender with a 4-year award (cancellable after 2.5 years) at a headline $390k dayrate, although when accounting for a required Managed Pressure Drilling (MPD) upgrade requiring as much as $30mm, the clean dayrate is estimated at approximately $370k/day after accounting for the MPD upgrade cost. Notably, as a locally based driller in Brazil, the $370k dayrate should generate stronger cash margins for Constellation than an international driller would achieve given its lower cost structure.

As a part of Petrobras’ Renecon, two 7G drillships had modest dayrate reductions in exchange for existing contract extensions. Eldorado Drilling’s 7G Atlantic Zonda had a 365-day extension (to 2Q29) at a net $397k dayrate when adjusting for the rate reduction across the extended contract period. Transocean’s 7G+ Deepwater Aquila also had a similarly structured 365-day extension through June 2028 at a net dayrate of $411k. Notably, Aquila is an enhanced hookload capacity drillship accounting for a modestly higher dayrate than Zonda.

In December 2025, Valaris announced an 800-day contract award for 7G DS-8 in Brazil at a $375k dayrate, which was viewed as a relatively soft rate at the time, and appropriately so considering Zonda and Aquila’s $397k and $411k dayrates, respectively, and higher rates in other parts of the globe.

6G Drillships and Semisubs: Long-Term Utilization Over Dayrate

The regional drillers in Brazil tend to have fleets comprised mostly of 6G rigs and value long-term utilization. Brazilian regionals Foresea (ODN I), Constellation (Alpha Star) and Ventura (SSV Victoria) all had multiyear contract awards for 6G’s with estimated clean dayrates in the $280k-$300k range. As Brazilian regionals, their lower cost structures result in lower headline dayrates, though on an internationally comparable basis, effective rates would be in the mid-$300k range, consistent with Transocean’s Orion award.

Transocean’s 6G Deepwater Orion received a 1,095-day contract extension keeping the rig working through March 2030, coupled with a dayrate reduction for a 340-day period beginning April 1, 2026. Adjusting for the rate reduction, Orion’s blended dayrate of approximately $365k is comparable to other Brazilian 6G awards on a margin-adjusted basis, accounting for Transocean’s higher international cost structure. As a lower-tier asset in Transocean’s fleet operating in a market with abundant comparable specification rigs, Orion faces meaningful competition — leading Transocean to prioritize long-term utilization over dayrate maximization, a rational strategy for an asset unlikely to command premium pricing in the current Brazilian market.

Constellation’s Gold Star semisubmersible secured a 2-year, 10-month contract at a $257k headline dayrate, though required equipment upgrades will reduce the adjusted dayrate further. The contract also includes a notable payment deferral, earnings through December 2027 are not due in cash until January 2028, and while Constellation is pursuing a factoring arrangement to accelerate cash receipts, this will come at a cost. The planned upgrades will orient Gold Star toward workover, intervention and plug-and-abandonment operations, mirroring the work profile of Constellation’s Atlantic Star. However, the non-cash impairment charge taken on Atlantic Star in 4Q25 raises questions about that rig’s long-term marketability and if Gold Star eventually fills a similar role in Brazil.

Ventura Offshore

Ventura Offshore is a small Oslo-listed driller with three owned rigs and one managed. Its SSV Victoria secured a 4-year Búzios contract (cancelable after 2.5 years) at a $320k headline dayrate, though a required MPD upgrade reduces the adjusted dayrate to approximately $290k — and potentially lower if mob fee impacts are relevant. Combined with Carolina’s existing $370k/day contract running into 2Q29, the two rigs should generate approximately $130mm of annual EBITDA in 2027-2028.

However, both rigs carry significant near-term capital requirements. Victoria requires a $25-$30mm MPD upgrade (payable in 1Q27) and $50-$54mm SPS, Carolina faces a $21-$24mm SPS ahead of its 911-day contract start in 2Q26, and fleet-wide spare parts add up to $19mm, bringing total capex to approximately $120mm. Against $43mm of cash and $135mm of debt at year-end 2025 — including a 10% coupon bond maturing April 2027 requiring $40mm of annual amortization — Ventura faces a funding gap of approximately $100mm beyond available liquidity, all else equal.

The addition of $466mm of new backlog from Victoria meaningfully strengthens Ventura’s refinancing position ahead of the April 2027 bond maturity, and the company has reportedly received several attractive refinancing proposals. Incremental debt capacity exists, though creditors may view gross debt above $200mm as too aggressive without meaningful amortization requirements, particularly given the uncertain earnings contribution from the uncontracted SSV Catarina after 2Q26 and potential warm-stacking costs. Speculatively, Ventura appears likely to raise new equity (perhaps ~10% of current market cap) to cover funding needs (including debt service) and to support a bond refinancing, with hypothetical potential for hybrid capital structured with PIK optionality to preserve near-term cash flow while limiting dilution, although various financing strategies are being considered. Ventura has yet to announce a financing solution and will be one of the more interesting situations to monitor in the small-cap driller space.

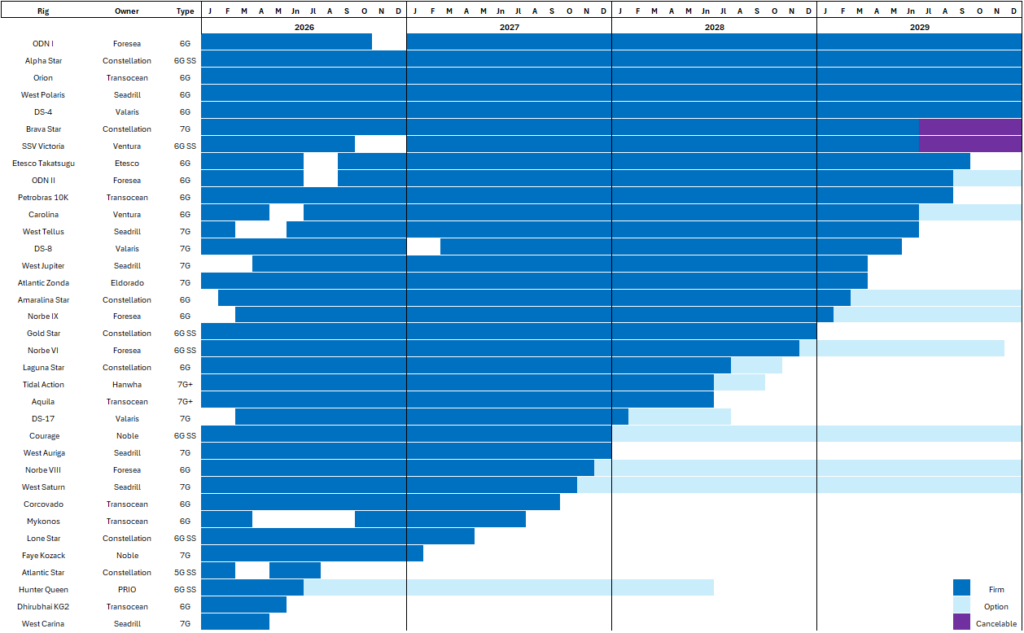

The picture below notes current contract timeline of deepwater rigs in Brazil as of April 6, 2026.

Comments (0)

Log in to leave a comment

Sign in