The two different fleets of Transocean and Valaris underscore the complementary nature of their proposed merger. The key differences are Transocean’s seven Norway-eligible semisubs – an asset class absent from Valaris’ fleet – and Valaris’ ~35-unit jackup fleet, which Transocean lacks entirely.

Comparatively, a hypothetical Valaris-Noble combination would combine two more similar, 7G drillship-heavy fleets. The chart below compares the fleet composition of six larger players, although other drillers exist including Saipem, Stena, Foresea, Eldorado and others. Also, NOC’s such as TPAO (Turkey) and Sonangol (Angola) own their own fleets.

If the Transocean-Valaris merger is approved, a common question is what Transocean should do with the jackup fleet? Contract drillers are similar to equipment rental businesses, and like financial entities, their equity value creation comes down to their ability to earn returns on their assets that exceed their cost of capital. Transocean retaining VAL’s jackups post-merger could be a meaningful lever in lowering its cost of capital: the geographic diversification into shallow water markets provides more stable through-the-cycle cash flows, which rating agencies and credit investors reward with lower financing costs, ultimately compressing the cost of capital and improving returns to equity.

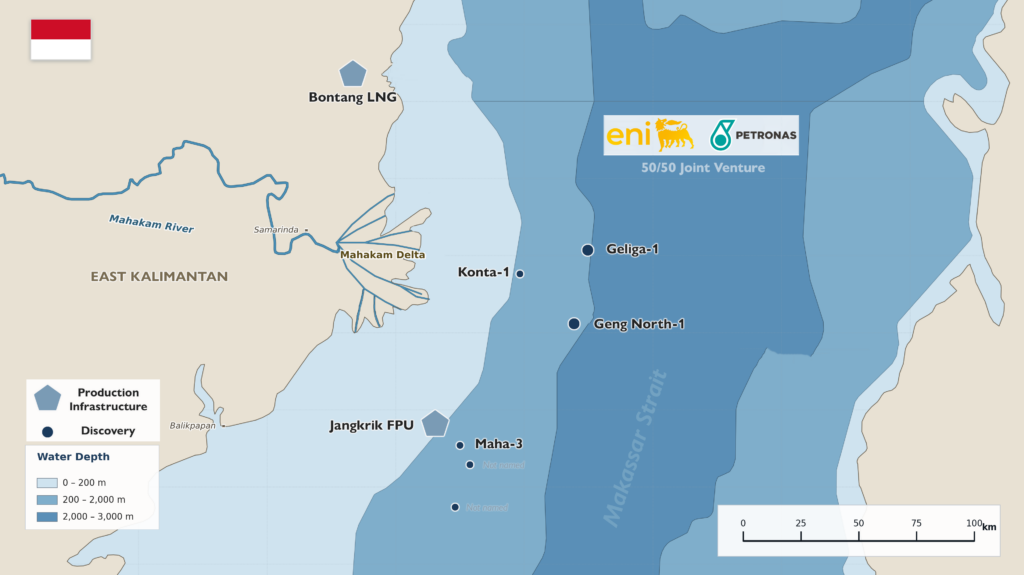

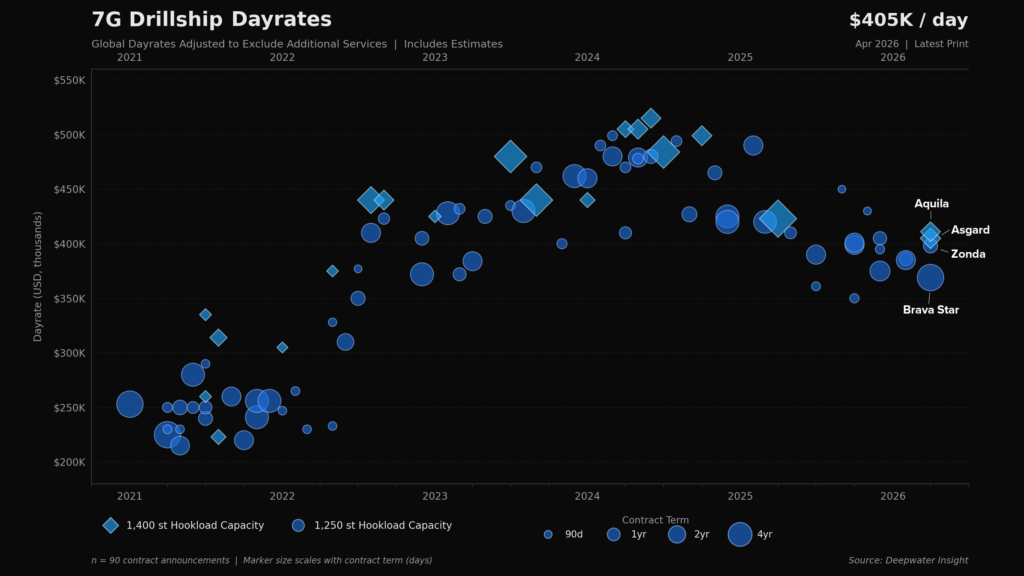

After navigating soft demand conditions from 2025-1H26, the market recovery is materializing broadly as anticipated. The drillship market has several multiyear tenders representing incremental demand — notably Indonesia, as well as Mozambique and Namibia where formal FIDs have yet to be taken but are likely. While awaiting regulatory approval on the Transocean merger, Valaris is likely marketing one or two of its cold, “stranded newbuild” 7G drillships, DS-13 and DS-14, acquired in Dec ‘23 for $337 million via purchase options negotiated with the shipyard during Valaris’ bankruptcy process in 2020-2021.

A key question on TotalEnergies’ two-rig Namibia (Venus) tender will be if they choose to use a harsh environment semisub (Northern Ocean’s Deepsea Mira) or two drillships? Namibia can have seasonally harsh environment conditions but drillships are capable of operating in the environment. Deepsea Mira is a candidate for Total’s upcoming Mopane 2-3 well appraisal campaign in Namibia likely commencing in 4-5 months. In December 2025, TotalEnergies farmed into Galp Energia’s PEL 83 license, acquiring a 40% operated interest following Galp’s Mopane discoveries and 10 billion boe in-place resource estimate. Galp retained the remaining 40% after originally holding an 80% working interest.”

Seadrill’s 1Q26 Conference Call Review

In March 2026, Seadrill appointed Samir Ali as CEO, replacing Simon Johnson who had been CEO since March 2022. Seadrill has struggled to generate positive free cash flow since 2024, but its 1Q26 earnings call signaled an appropriate shift in focus — targeting sustained free cash flow generation in 2H26 and beyond as the foundation for recurring shareholder returns.

One of the first tangible steps was securing new contract awards for 7G drillships West Neptune and West Vela with LLOG/Harbour Energy in the US Gulf. LLOG’s addition of a second Seadrill rig following Harbour Energy’s acquisition was a positive demand signal, although the high-$300k dayrate prints — likely inclusive of MPD — were softer compared to the ~$400k market for 7G drillships. As Seadrill flagged on its 1Q26 call, prioritizing utilization over rate to achieve free cash flow inflection is a defensible trade-off at this stage of the cycle.

Seadrill’s prior CEO noted the strength of the Norwegian E&P market on a recent conference call but did not mention Seadrill’s two Norway-eligible semisubs, Phoenix and Aquarius, were cold-stacked with each requiring well over $100mm in reactivation capex and to meet Norway’s regulatory standards. Despite the strength of the Norway E&P market, Seadrill noted on its 1Q26 conference call it would not reactivate either rig unless a customer funds the reactivation. A ~$150 million reactivation spend on either rig would be directly at odds with Seadrill’s stated free cash flow objectives and is therefore very unlikely in the next 12-18 months.

Comments (0)

Log in to leave a comment

Sign in