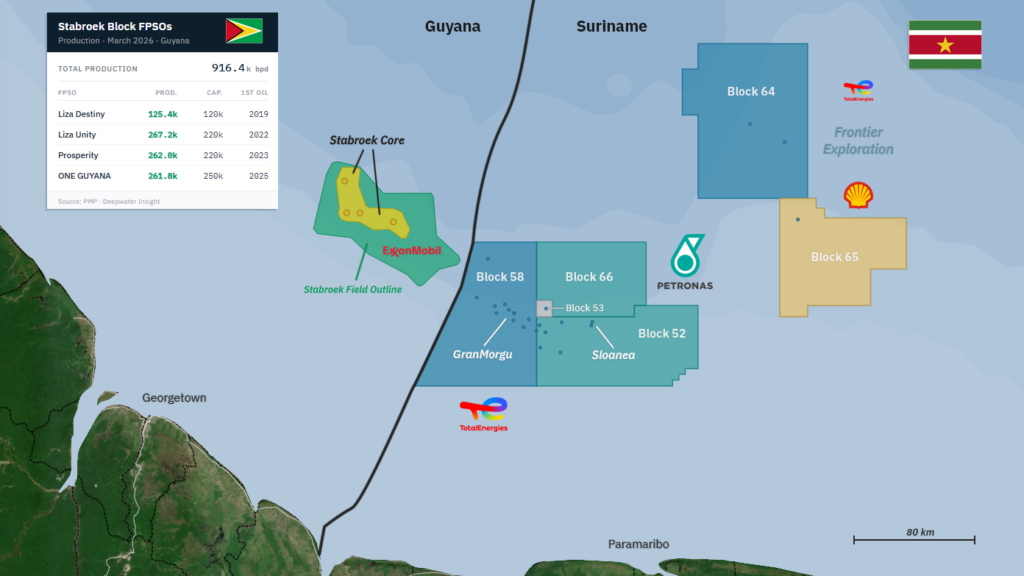

Suriname, Guyana’s eastern neighbor, is on the cusp of its own energy transformation. GranMorgu, a 220k bpd oil project targeting first oil in 2028, nascent FLNG prospects and an active exploration campaign that will define whether its energy future is crude oil, FLNG or both.

TotalEnergies began exploring in Suriname in 2020 after a Block 58 farm-in agreement with APA in 2019. The process proved more challenging than Exxon’s in Guyana, as Block 58 discoveries tended to have higher gas content. Despite some challenges, TotalEnergies discovered enough recoverable oil to FID GranMorgu, a $10.5B, 220k bpd oil project. TotalEnergies and Shell also have frontier exploration potential in Blocks 64 and 65 about >200 km NE of GranMorgu.

Guyana’s Stabroek core is expanding, although still ~100 km NW from GranMorgu, where reservoirs have demonstrated to be comparatively higher gas content.

In Block 52, Petronas (80%) and Staatsolie (20%) declared the Sloanea gas discovery commercial after appraisal. Over 150 km east of Guyana’s Stabroek core, Sloanea is a high-quality dry gas reservoir with FLNG export potential. Block 52 has also had oil discoveries to the west, although not yet enough to justify its own development. Petronas is expected to drill two exploration wells in Block 66, likely in 2027, which could identify another oil discovery it could add to Fusaea and Roystonea for a potential oil development, or discover more dry gas like Sloanea for more FLNG export potential.

Suriname’s entire 2025 GDP of $4.7 billion is less than half the $10.5 billion FID taken on Block 58 alone — underscoring the transformative potential of offshore oil and LNG for the country and its vulnerability to commodity market volatility.

Suriname’s NOC, Staatsolie, holds 20% interests in both Block 58 and Block 52 (Sloanea FLNG), funding its share of capex likely through debt markets given Suriname’s limited fiscal resources. FLNG is a natural fit for Suriname — by selling its production entitlement under long-term fixed-price contracts to investment grade utility counterparties, Staatsolie can convert volatile commodity prices into a steady, infrastructure-like revenue stream for stronger economic stability.

In November 2020, Suriname defaulted on its sovereign debt. Three years later, it exited default by issuing new debt with oil-linked Value Recovery Instruments (VRIs) — entitling bondholders to a portion of Block 58 royalty payments (6.25%) as a restructuring settlement. The VRIs served as a credit enhancement and moved bond holders closer to cash flows, with bondholders receiving partial exposure to Block 58 royalty cash flows on top of their restructured debt claim. Notably, while ceding royalty exposure to distressed bondholders raised questions about resource sovereignty, Suriname retained a call option to redeem both the bonds and VRIs at any time.

In a positive development, Suriname redeemed its VRIs, meaning the 6.25% Block 58 royalties will flow to Suriname rather than foreign bondholders when GranMorgu produces first oil in 2028. The redemption was costly, but the VRIs were a product of Suriname’s prior fiscal distress. With them retired, Suriname now retains its full royalty stream plus 20% of oil profit through Staatsolie’s working interest in Block 58. Staatsolie also holds 20% in Block 52’s Sloanea dry gas discovery, recently declared commercial by operator Petronas.

Staatsolie is an intriguing, new high yield, emerging market credit issuer. While Suriname (Caa1/CCC+) has a challenging history, its economy is on the cusp of transformation with its national oil company Staatsolie at the center. In 2025, Staatsolie produced only 17.4k bpd — a figure set to grow dramatically as its 20% share of GranMorgu contributes 44k bpd at peak. Beyond GranMorgu and Sloanea, Staatsolie also holds a diversifying 25% interest in a Newmont-operated gold mine.

Staatsolie is funding its 20% working interest in the $10.5 billion GranMorgu development — benefiting from TotalEnergies’ operatorship on what is a technically complex project. To finance its share of capex, Staatsolie raised capital through a dual-currency bond offering and a syndicated loan, pricing a USD-denominated tranche at 7.75% and a EUR-denominated tranche at 7.25%. In late 2025, Petronas and Staatsolie declared the Sloanea gas discovery commercial, likely paving the way for a late-2026 FID. Investment in Sloanea would represent another meaningful capex commitment for Staatsolie, with further funding requirements depending on exploration and appraisal outcomes across its other blocks.

Comments (0)

Log in to leave a comment

Sign in